A Better Way Financial

Empower Your Retirement

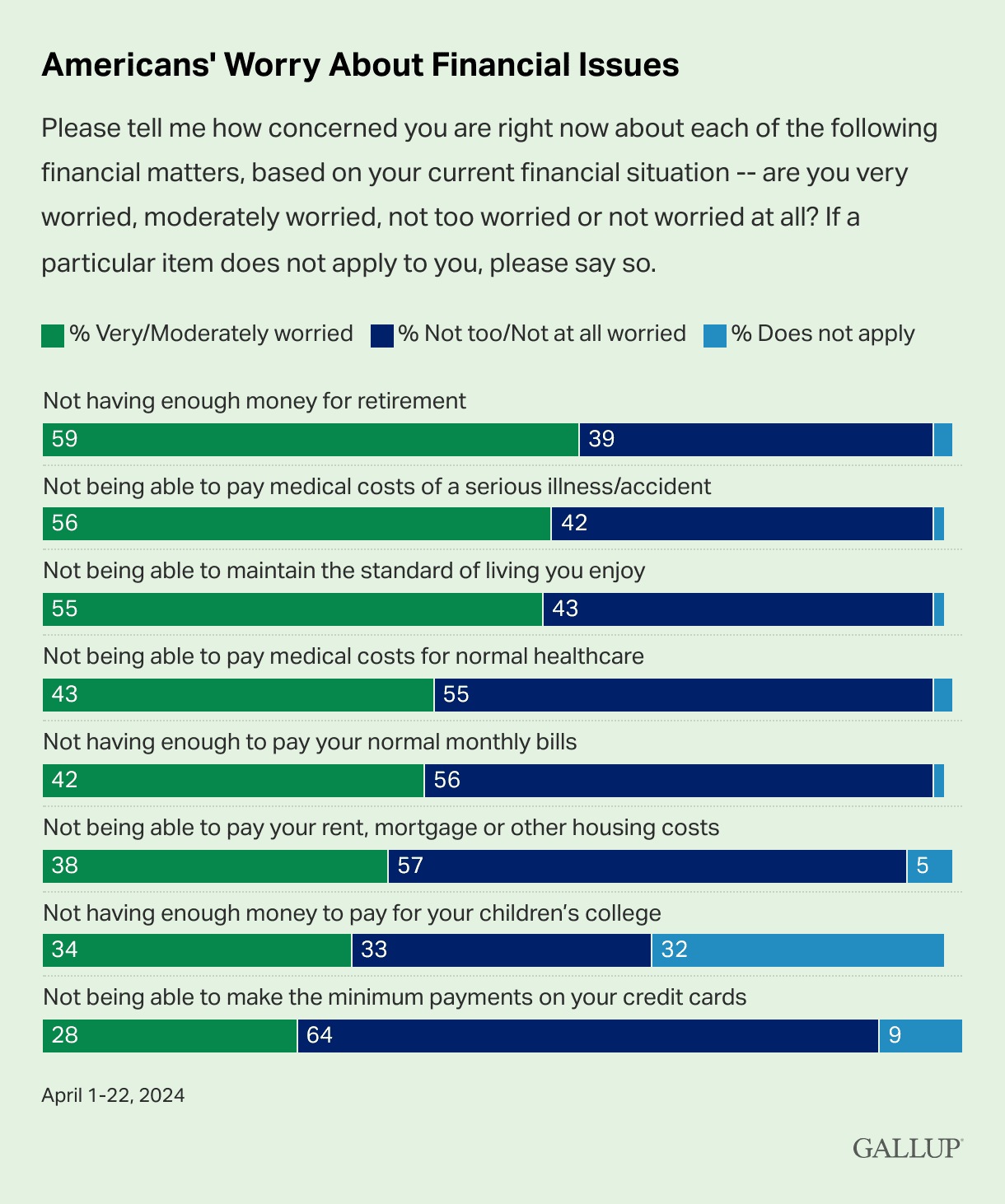

According to a poll conducted by Gallup, nearly 60% of Americans believe they haven’t saved enough for their retirement. Over half stated that they are afraid they won’t be able to maintain their current standard of living once they retire. [1] This brings us to the question of how you determine if you have enough retirement savings, and what challenges you may face when you start withdrawing from your savings in retirement.

One of the most significant concerns for retirees is inflation. According to the same Gallup poll mentioned earlier, 41% of Americans named inflation as the most important financial problem facing their families today. This was by far the most popular answer, with the next most popular answer being the cost of owning/renting a home. Only 14% of respondents chose that as their biggest financial problem.

The reason inflation can be a huge problem during your retirement is that it can silently erode the purchasing power of your money. What seems like a substantial amount today might not be sufficient in the future. For example, if you need $100,000 in income today, assuming an annual average inflation rate of approximately 2.4%, you will need $200,000 in income in 30 years to maintain the same standard of living.

Ensuring that your income increases with inflation is crucial to preserving your purchasing power. This requires careful planning and investment strategies that account for the rising cost of living.

Another major concern for retirees is taxes. Without a proper tax plan, you could face significant tax bills in retirement due to required minimum distributions (RMDs) from pre-tax IRAs or 401(k)s. RMDs are the minimum amounts you must withdraw from your retirement accounts each year. You generally must start taking withdrawals from your traditional IRA, SEP IRA, SIMPLE IRA, and retirement plan accounts when you reach age 72 (73 if you reach age 72 after Dec. 31, 2022). [2]

According to The Motley Fool, 60% of Americans have retirement money saved in pre-tax accounts such as 401(k)s and IRAs [3]. This means they chose to delay being taxed on the money they contributed until they eventually withdraw the money from the account(s). The general idea behind this strategy is that they hope to be in a lower tax bracket in retirement when they need the money than they were when they earned it during their working years. However, RMDs can mess up that math.

These mandatory withdrawals can push you into higher tax brackets, increasing your tax burden at a time when you’re trying to manage your income carefully. Proactive tax planning can help mitigate these issues, ensuring you retain more of your money and reduce the impact of taxes on your retirement income.

Determining if you have enough money saved for retirement isn’t a simple question with a straightforward answer. It involves evaluating several factors:

To figure out if you have enough put away in retirement savings, you need to consider your anticipated expenses and match them against your income sources. If you need $50,000 annually, do your savings and income sources meet this need? With proper planning, you might even exceed this amount, providing greater financial security and peace of mind.

Understanding these factors and planning accordingly can help ensure you have the income you need throughout your retirement. If you want to learn more about retirement planning, fill out the form below to get in touch with us today!

[1] https://news.gallup.com/poll/644690/americans-continue-name-inflation-top-financial-problem.aspx

[2] https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

[3] https://www.fool.com/research/average-retirement-savings/

*Your privacy matters. All information is kept secure and confidential.

"*" indicates required fields