A Better Way Financial

Empower Your Retirement

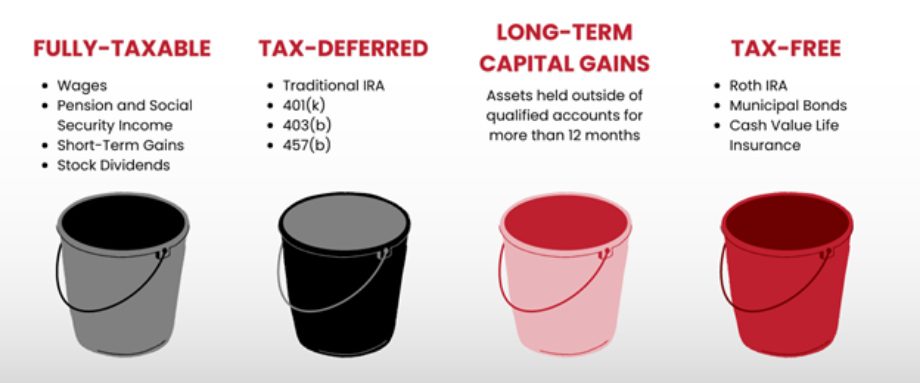

When it comes to retirement planning, understanding how taxes work can make a significant difference in the amount of money you end up with. There are four different tax buckets to consider when planning for retirement, each with its own tax implications.

The first tax bucket is your fully taxable bucket. This includes any income you have coming in, such as Social Security income, pension income, rental real estate income, salary, bonuses, wages, and income from 1099 employment. All of these are taxed at ordinary income tax rates. Short-term securities or mutual funds held for less than one year are also taxed at ordinary income tax rates.

The second bucket is the tax-deferred bucket, which includes contributions to 401(k)s, 403(b)s, and 457s, as well as traditional IRAs. Contributions to these accounts give you a tax deduction in the year you make them, but the money grows tax-deferred until you withdraw it in retirement. At that point, you’ll have to pay ordinary income taxes on the funds, which can create a significant tax bill.

The third bucket is the long-term capital gains bucket. If you hold an asset, such as stock or real estate, for more than one year before selling it, you’ll enjoy a lower long-term capital gains tax rate. The tax rate for long-term capital gains is generally lower than the ordinary income tax rate, which can save you money. However, there are income thresholds for paying long-term capital gains taxes.

The fourth and final bucket is the tax-free bucket, which includes Roth accounts, cash value life insurance, and municipal bonds. Roth accounts, such as Roth IRAs and Roth 401(k)s, allow your contributions to grow tax-free, so you don’t pay taxes on the growth or when you withdraw the money in retirement. Cash-value life insurance allows you to put in taxable dollars and take them out tax-free later in retirement, while municipal bonds provide tax-free interest and sometimes state income tax-free interest.

Of all these buckets, the tax-free bucket is the most desirable since it allows your money to grow tax-free. A strategy to consider when looking to maximize your tax-free savings in retirement is Roth conversions. This is a strategy where you convert money from a traditional IRA or 401(k) to a Roth IRA. You’ll have to pay taxes on the amount you convert, but once the money is in the Roth IRA, it can grow tax-free. Over your lifetime, this can save you hundreds of thousands of dollars in taxes.

We often get asked, “Why would I pay the tax now if I could wait and pay it later?” When looking at doing Roth conversions and paying taxes sooner rather than later, it is important to understand the Rule of 72. This rule is a quick and easy way to estimate how long it will take for your investments to double in value. To use the Rule of 72, simply divide the number 72 by the annual rate of return on your investments. The result is the approximate number of years it will take for your investments to double in value.

For example, if your investments have an annual return of 8%, it will take approximately 9 years (72 divided by 8) for your investments to double in value.

To further this example, let’s say you take $100,000 and invest it in a 401(k) or a traditional IRA. If you get an 8% annual return on that $100,000, it will quadruple to $400,000 in 18 years. When you go to withdraw that money, you are now paying taxes on $400,000 instead of $100,000.

With Roth conversions, you would pay taxes on the $100,000, letting it grow tax-free over those same 18 years, giving you $400,000 of tax-free money, or $300,000 of tax-free growth on that original $100,000. This begs the question: would you rather pay taxes on the seed (the $100,000) or the harvest (the $400,000)?

Keep in mind that Roth conversions don’t make sense for everyone. It is important to talk to a financial professional to see if Roth conversions make sense for you. At A Better Way Financial, we have helped people across the country understand whether a Roth conversion strategy can help them save on taxes in their retirement. To learn more about how A Better Way Financial can help you with tax planning for your retirement, fill out the form below.

*Your privacy matters. All information is kept secure and confidential.

"*" indicates required fields