A Better Way Financial

Empower Your Retirement

We’re always looking for ways to improve our retirement strategy. One tool we hear a lot about these days is the Roth IRA. Wealth manager Winnie Sun tells Forbes that it’s the “golden egg of retirement accounts.” [1] This sounds like a great endorsement but are Roth IRAs always the best choice?

Understanding whether a Roth IRA is right for you starts with understanding whether you qualify. Not everybody knows exactly what that means, so let’s look at the qualifiers.

If you earn above a certain income threshold, you will not qualify to put a dollar into a Roth IRA. In 2022, these thresholds are $214,000 if you are married filing jointly or $144,000 as a single tax filer. If you contribute to a Roth IRA after surpassing these thresholds, the IRS will come knocking on your door and ask why you’re putting money into the Roth IRA. However, if you make less than those thresholds, then a Roth IRA may be a good investment.

The first requirement is to ensure you don’t exceed a certain income threshold. The second is that you must have earned income. What does that mean? Earned income is any income that is received as a result of paid work. This can include your hourly wage, salary, tips, and bonuses from your job, as well as earned income from a business you operate.

So, what if you’re already retired and/or your only source of income is Social Security, rental real estate property, investments, and the like? Well, these do not qualify as earned income. Therefore, you wouldn’t be able to invest any money in a Roth IRA. The only way you would be able to do that would be through a Roth conversion, which we utilize very frequently here at A Better Way Financial. We’ll touch on that more toward the end of the article.

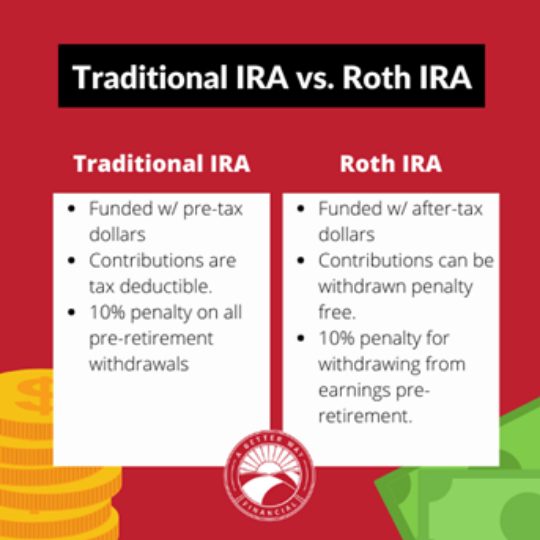

Many people approaching or at retirement age today are familiar with a traditional IRA, but what is the difference between this investment vehicle and a Roth IRA? And, more importantly, when is a Roth IRA a better choice over a traditional IRA?

A lot of the people we sit with for their complimentary tax and retirement review have a traditional IRA. The reason for this is that traditional IRAs provide a tax deduction in the year that you contribute to them. They’ve been told to contribute to their traditional IRA throughout their working years, thinking that their income at that time will be higher than it will be in retirement since they will no longer be earning a living. However, we have found this to be a common myth.

It’s often thought that by the time you retire, your expenses will drastically decrease; expenses like your mortgage will be paid off, and you’ll have fewer bills in general, meaning you’ll be able to live on less money. However, this is often not the case, thanks to inflation. The cost of goods continues to rise throughout your retirement years, meaning you’ll pay more for everything else you purchase. This can cause you to pull more and more every year from your retirement savings as income, potentially keeping you in the same higher tax bracket that you were in during your working years.

When you contribute money to a Roth IRA, you don’t get the tax deduction for that year. However, any growth that you get on that money continues to grow tax-free for the rest of your life. Looking at it from a long-term perspective, the tax savings here can be tremendous.

At A Better Way Financial, we believe that in your retirement, it is better to “pay taxes on the seed rather than on the harvest”. When it makes sense to do so, utilizing a Roth IRA to turn the growth on your investment into tax-free income can be a very powerful retirement tool.

If you are approaching retirement or are already retired, contributing to a Roth IRA can be a great way to generate tax-free income. However, does it always make sense to do so?

Converting your traditional IRA into a Roth IRA is typically a good idea when you believe that tax rates will be lower today than they will be in the future. Looking at the situation right now in 2022, it is a wonderful time to go into a Roth IRA if you can. This is primarily because the tax rates are lower now than they will be in the future, since they are currently scheduled to go up in 2026. This means that now through 2025, taxes are essentially “on sale”. Depending on your situation, it can be better to pay the taxes now, do the ROTH conversions, and let that Roth IRA money grow for you tax-free into retirement and beyond.

If you’d like to learn more about whether converting to a Roth IRA is best for you, fill out the form below or give our office a call at (610) 400-1700 and speak to one of our fiduciary financial planners.

[1] Sun, W. (2022, April 21). Why you should be considering the Roth IRA this year. Forbes. Retrieved May 4, 2022, from https://www.forbes.com/sites/winniesun/2021/11/08/why-you-should-be-considering-the-roth-ira-this-year/?sh=7e02a9154e56

[2] Schneider, J. (2021). 2022 Income Limits. Personal Finance Club. Retrieved May 4, 2022, from https://www.personalfinanceclub.com/wp-content/uploads/2021/11/2021-11-12-2022-Roth-IRA-Income-Limits-1024×1024.png.

*Your privacy matters. All information is kept secure and confidential.

"*" indicates required fields